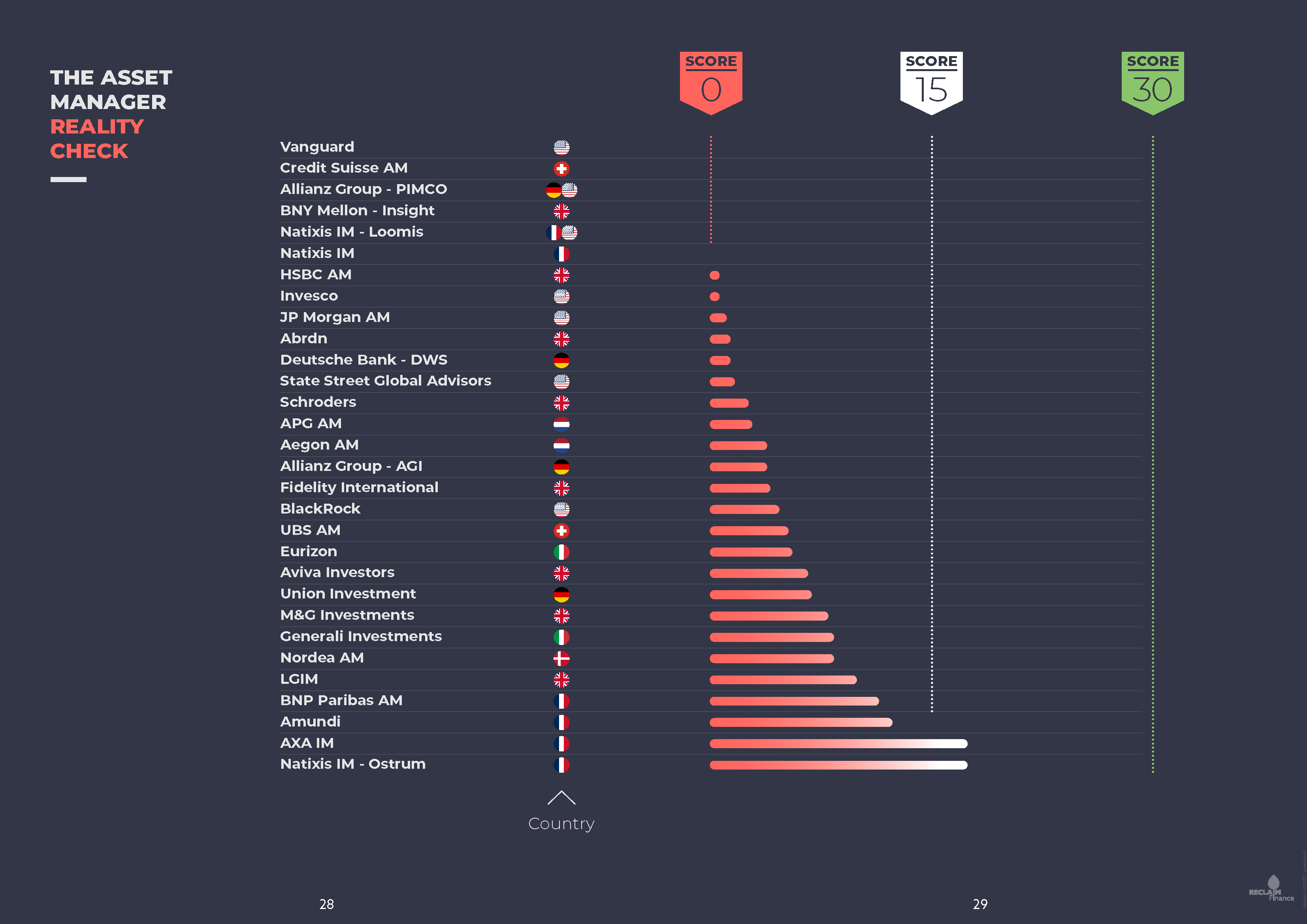

Reclaim Finance, The Sunrise Project, Re:Common and Urgewald have released a scorecard ranking 30 major asset managers on their climate commitments, with a focus on their approach to the fossil fuel sector. The analysis provides new data on their exposure to companies with the biggest fossil fuel expansion plans.

Of the 30 asset managers that were assessed, 25 are members of the Net Zero Asset Manager Initiative (NZAM). Yet not a single one of them has set the expectation that companies in their portfolios should quit developing new coal, oil or gas projects in line with climate science. NGOs call on asset managers to urgently restrict investments in fossil fuel expansion and to vote against coal, oil, and gas expansionists during the upcoming AGM season.

Big exposure and small-scale action

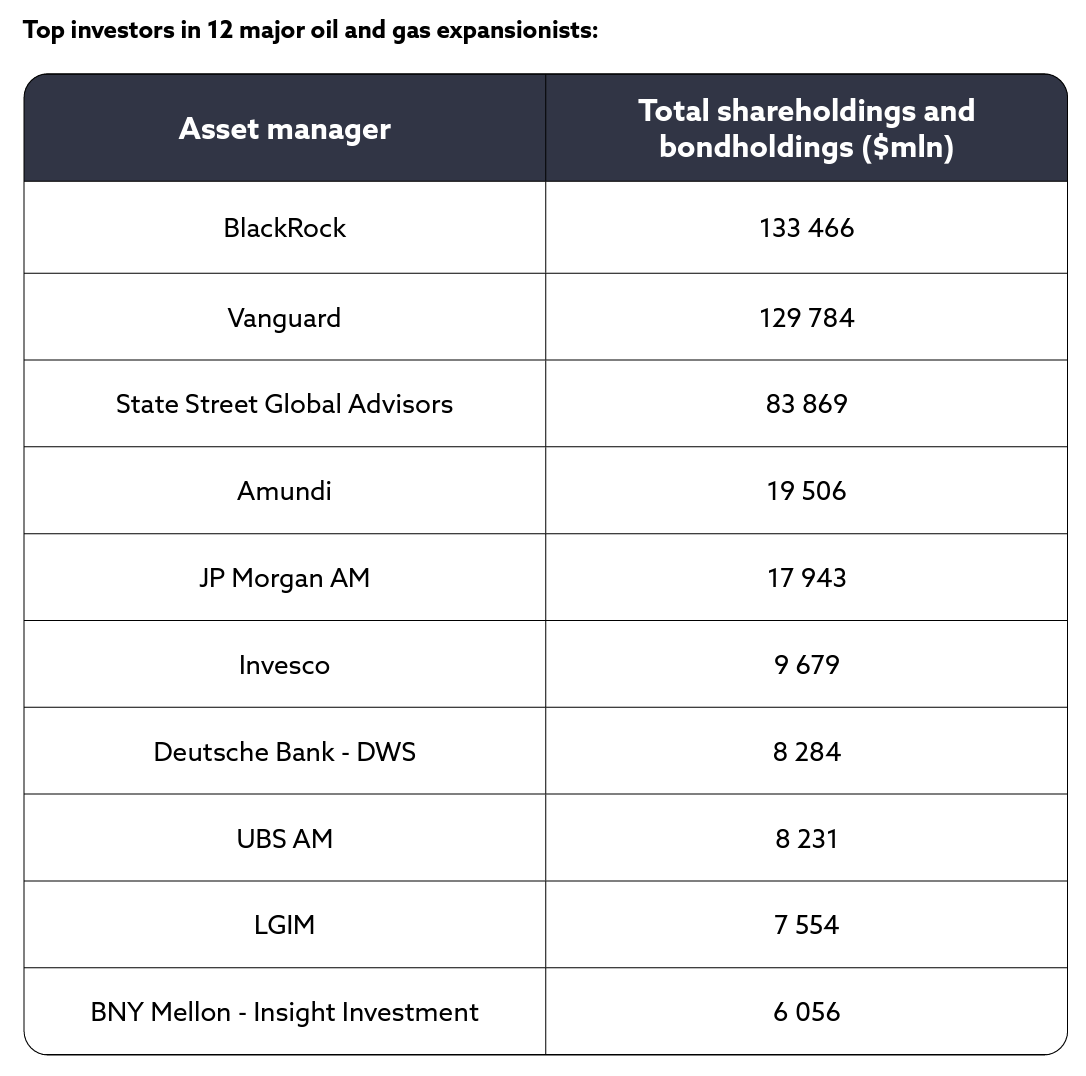

The 30 asset managers assessed hold more than $82 billion in companies developing new coal projects. The numbers are even more staggering for the oil & gas industry: together, the 30 asset managers hold $468bn in 12 major oil and gas companies with massive upstream expansion plans.

The report finds that their policies and investment guidelines, due to vague criteria that leave the door open for the worst polluters, are too flawed for the asset managers to align their entire portfolios with a net zero target.

17 asset managers now have a coal policy and 12 have an oil and gas policy. Vanguard, State Street Global Advisors and Allianz’s asset management branch PIMCO are among the biggest firms with no fossil policy at all.

Among the asset managers with policies, only seven restrict investments in companies developing new coal projects, a number that hasn’t changed since last year, and none restrict investments in companies developing new oil and gas supply projects. More and more policies introduce exceptions to exclusion criteria. For instance, among the seven asset managers that restrict investments in companies developing new coal projects, three plan to introduce undefined exceptions to this rule. Even more worryingly, scrutiny reveals a growing trend of policies and targets that apply only to a small share of the asset managers’ assets.

None of the asset managers apply their existing fossil fuel restrictions to all their ‘passively’ managed assets, which is particularly concerning considering ‘passive’ investments keep growing and represent 46% of the assets covered by the report. The nine biggest ‘passive’ asset managers within our sample of 30, are also among the biggest holders of companies developing new coal projects. This is due to none of them applying robust coal criteria to their ‘passive’ funds. Ten of the asset managers have released 2030 decarbonization targets, however, the targets only cover a small share of their portfolios.

The deeply disappointing findings revealed in the scorecard are published one day ahead of the one-year anniversary of the Glasgow Financial Alliance for Net Zero (GFANZ). The results are a testament to the alliance’s lack of effectiveness, with prominent members such as Vanguard, Credit Suisse and PIMCO identified among the main laggards.

“Is the asset management industry changing its investment practices in line with climate science, reducing investments in coal, oil, or gas expansion? Unfortunately, the answer is an emphatic “no”. Leading asset managers are kicking the can down the road without even asking companies to stop worsening the climate crisis. Let’s be clear: drilling a new oil well or opening a new coal mine is not a normal thing to do in a widespread climate catastrophe. BlackRock most embodies the hypocrisy of too many asset managers: whilst being the biggest member of the NZAM, it still invests in the 11th biggest coal producer worldwide and massive coal expansionist Glencore.”

– Lara Cuvelier, Campaigner at Reclaim Finance

Asset managers are major bondholders in coal, oil and gas companies

Regarding the coal sector: out of the 30 asset managers listed in this report, BlackRock and Allianz Group are the biggest bondholders of coal companies with expansion plans. Neither of them has committed to denying new debt to companies involved in coal expansion (or even threatened to do so). Neither of them is using their bond power to ask that expansion stops, despite the fact that new coal projects are incompatible with a pathway consistent with the 1.5°C limit in the Paris Agreement.

Regarding the oil and gas sector: the selected asset managers are holding at least US$ 144bn in bonds issued by more than 300 oil and gas companies. Top bondholders include Blackrock and Vanguard which hold US$ 34bn each, as of March 2022. The third biggest bondholder is Allianz, with US$ 17bn in bonds held by its asset management branches PIMCO and Allianz GI.

Given the growing importance of corporate bond issuance in companies’ fund-raising strategies, it is particularly important for investors to be held accountable when they buy newly-issued bonds. For instance, in 2019, JP Morgan and Schroders bought US$ 18mn and US$ 4mn respectively in a bond issued by Pemex (Petroleos Mexicanos), a major oil and gas producer that specializes in extra heavy oil and offshore extraction projects (and is sadly renowned for provoking offshore fires). That same year, BlackRock, Natixis and Invesco bought US$ 36mn, US$ 10mn and US$ 8mn respectively in a bond issued by Saudi Aramco, the 2nd biggest producer and 3rd biggest developer of oil and gas globally.

Divest or engage: a false debate?

The scorecard also analyzes asset managers’ specific requests and escalation strategies towards fossil fuel companies. Despite being very vocal about virtues of engagement to generate climate impact (11), asset managers’ soft and largely unstructured dialogue with fossil fuel companies failed to stop them from developing new oil and gas fields.

25 asset managers state that they engage companies to push for improvements on climate-related issues but none call for a decrease of companies’ overall fossil fuel production or a stop to all new fossil fuel supply projects.

None of the 30 asset managers have clear and comprehensive demands, whilst only eight publicly ask companies to adopt short-term emission reduction targets.

The absence of specific requests, matched by credible sanctions, makes engagement activities mostly toothless and ineffective. The six European oil and gas majors, which claim to be the best-in-class of their sector in terms of transitioning their activity, are a case in point. A case study in the report describes their massive expansion plans and misalignment with Paris Agreement goals, illustrating the consequences of investors’ failed engagement towards them. BP, for example, will have used up its entire carbon budget to stay below 1.5°C by 2033 – a fact that does not seem to have warranted pushback from asset managers.

“This confirms that the “divestment versus engagement” debate is a big distraction. Asset managers are not engaging companies on the key climate issues when it comes to limiting global warming to 1.5°C. It’s also striking that they are actually sending the opposite signal because they are still buying new debt from fossil fuel developers. Asset managers that provide fresh cash to companies that are ignoring climate science are purely and simply pouring more fuel in the fire.”

– Lara Cuvelier, Campaigner at Reclaim Finance

The report calls on asset managers to finally adopt robust exclusion and engagement policies to tackle fossil fuel expansion, which in practice means that they should be asking their clients to give up their expansion plans, escalate against those who fail meeting this demand, and be ready to divest from them after a short deadline.

Share